UK Bettors Draw Line at Bank Statements for Gambling Affordability Checks as Black Market Warnings Mount

UK Bettors Draw Line at Bank Statements for Gambling Affordability Checks as Black Market Warnings Mount

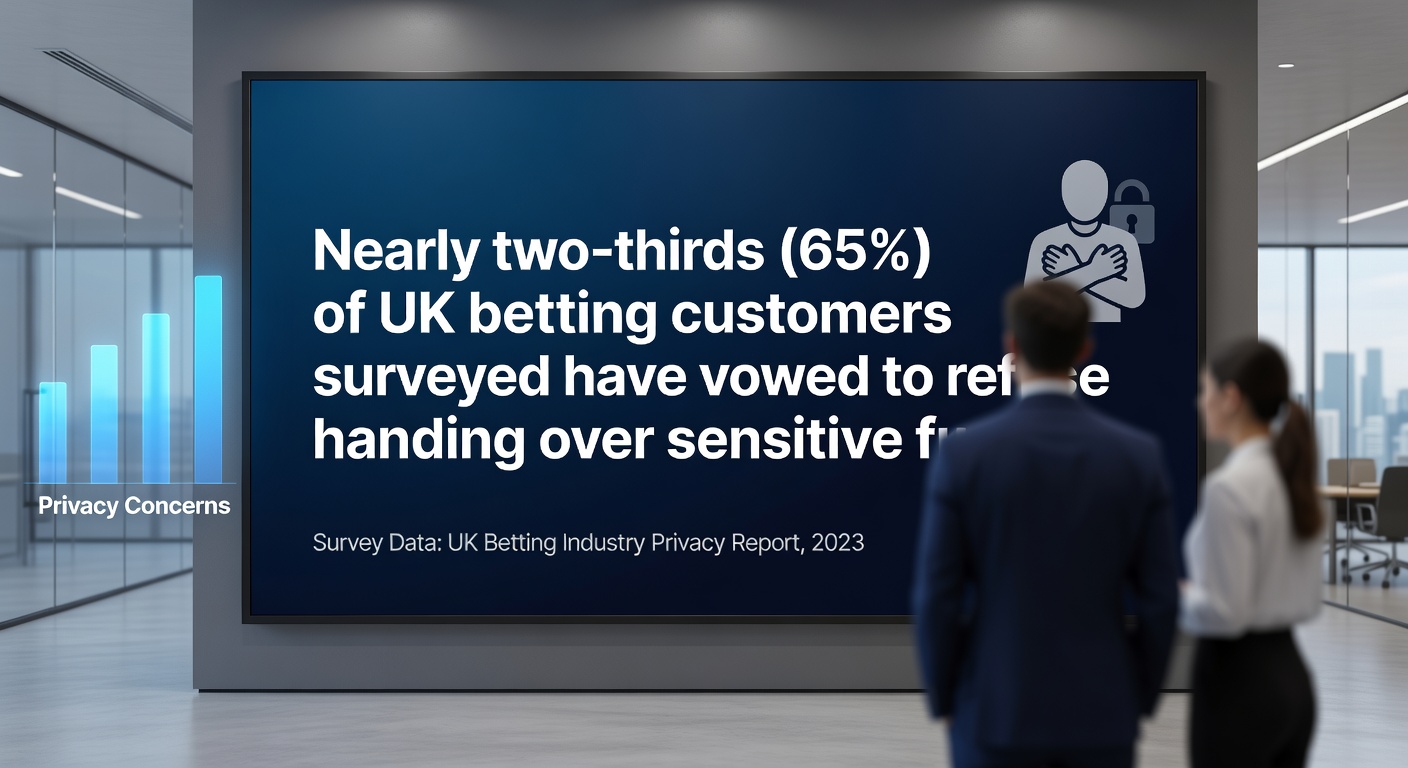

Punters' Strong Resistance Surfaces in Key Survey

A recent survey conducted by the Betting and Gaming Council polled over 2,000 UK betting customers, revealing that nearly two-thirds—precisely 65%—would outright refuse to submit bank statements or other financial documents demanded under the Gambling Commission's proposed online gambling affordability checks; these measures, modeled after mortgage affordability assessments, aim to verify bettors' financial capacity before allowing wagers, yet the data indicates widespread pushback from everyday punters who view such intrusions as crossing a privacy threshold too far.

What's interesting here is how this poll captures a snapshot of real sentiment among active bettors, many of whom frequent horse racing tracks or football matches, placing regular stakes without issue; researchers behind the survey noted that respondents cited concerns over data security and personal autonomy, with one common refrain being that sharing detailed transaction histories feels more invasive than standard age or identity verification processes already in place.

And while some participants expressed openness to lighter-touch checks—like self-reported income brackets— the overwhelming majority drew a hard line at handing over full bank records, a stance that underscores the tension brewing as these reforms edge closer to implementation in April 2026.

Gambling Commission's Research Reinforces the Divide

Separate research from the Gambling Commission itself, drawn from a larger pool of 12,000 frequent gamblers, paints an even starker picture: over three-quarters—75%—oppose the proposed affordability checks, echoing the Betting and Gaming Council's findings while amplifying the scale of discontent across a broader demographic of high-volume players.

This data emerges from structured interviews and questionnaires designed to gauge attitudes toward financial friction in online betting, where participants highlighted fears that rigorous document scrutiny could disrupt casual enjoyment without meaningfully curbing problem gambling; experts analyzing the results point out that frequent gamblers, often the lifeblood of platforms offering horse racing odds or in-play football markets, see these checks as a barrier that punishes responsible bettors alongside those in need of intervention.

Turns out, the Commission's own figures align closely with industry polls, suggesting a consensus among users that while player protection matters, the proposed methods—requiring proof of disposable income via statements or payslips—strike many as overly bureaucratic, potentially alienating loyal customers who've bet responsibly for years.

Racing Professionals Sound Alarm on Economic Fallout

Industry figures, including over 400 racing professionals such as trainers Lucinda Russell and Robert Waley-Cohen, have fired off a stark warning to Culture Secretary Lisa Nandy, arguing that these affordability checks could shove punters toward illegal black market operators; their letter projects devastating losses—£250 million to British horse racing and £200 million in vanished tax revenue—as regulated sites lose custom to unregulated alternatives that sidestep all verification hurdles.

Those who've studied the betting ecosystem note how horse racing relies heavily on steady wagering volumes from online punters, where even small shifts in behavior—like switching to offshore apps with lax rules—could ripple through stables, tracks, and levy-funded prize pots; one case highlighted by signatories involves mid-tier trainers who depend on consistent betting turnover to sustain operations, a fragile balance now at risk from what they call "unintended consequences" of well-meaning reforms.

But here's the thing: black market migration isn't hypothetical—past regulatory tightenings in other sectors have driven similar flows, and with April 2026 marking the timeline for these checks to roll out, racing stakeholders emphasize that the government's own affordability framework might inadvertently fuel the very underground economy it seeks to combat.

Unpacking the Proposed Mortgage-Style Assessments

The Gambling Commission's blueprint for affordability checks draws direct parallels to mortgage lending protocols, where applicants must furnish bank statements, salary slips, and expenditure details to prove they can service debts without strain; applied to gambling, this means operators would flag accounts for enhanced checks once betting hits certain thresholds—say, £1,000 monthly net deposits—prompting requests for financial proof before stakes can continue.

Data from pilot programs and consultations shows these assessments would tier by risk, starting with remote monitoring of deposit patterns and escalating to document demands for higher spenders, yet survey respondents balk at the precedent of treating a £50 horse racing each-way bet like a home loan application; observers point out that while the intent—to shield vulnerable players from unaffordable losses—holds merit, the mechanics clash with the spontaneous nature of sports betting, where punters chase value in fluctuating odds rather than commit to long-term financial exposure.

So, as operators gear up for compliance by April 2026, the reality is that tech integrations for automated checks already strain resources, and with punter surveys forecasting mass opt-outs, platforms face a dilemma: enforce strictly and watch volumes plummet, or loosen up and invite regulatory backlash.

Broader Ripples Through Betting Landscape

People in the industry often draw parallels to earlier stake caps on slots, where similar friction led to player churn without clear wins on harm reduction; here, the Betting and Gaming Council's poll of over 2,000 customers reveals not just refusal rates but also why—65% cite privacy erosion as the top gripe, followed by fears of delayed payouts or account freezes during verification waits, issues that could hit peak times like Cheltenham Festival or Premier League weekends hardest.

Yet the Gambling Commission's 12,000-gambler study adds nuance, finding that while opposition runs deep, a minority—around 20%—welcomes checks if they're quick and anonymized, hinting at room for hybrid models that blend AI-driven spend analytics with voluntary disclosures; researchers who've pored over this data suggest that without tweaks, the reforms risk fracturing trust between regulators, operators, and bettors, especially in sectors like horse racing where levy income hinges on total turnover.

Now, with racing pros' projections of £250 million in losses looming large—money that funds everything from jockey schemes to track maintenance—the ball's in the government's court to weigh player protection against economic stability, all as black market apps lurk ready to capitalize on any regulatory overreach.

Stakeholder Reactions and Path Forward

Trainers like Lucinda Russell, known for Grand National triumphs, and Robert Waley-Cohen have led the charge in rallying over 400 signatures, their open letter to Lisa Nandy framing the checks as a "disastrous own goal" that endangers an industry employing thousands; figures from the British Horseracing Authority back this up, estimating that even a 10-15% drop in online betting could trigger the £200 million tax shortfall, cascading into reduced government coffers from the remote gaming duty.

That's where the rubber meets the road: as consultations wrap and April 2026 deadlines firm up, operators scramble to build compliant systems—think API links to credit agencies for softer checks—yet surveys warn that hard document demands will deter the casual punter who sustains daily racing markets; one study participant summed it up bluntly, noting they'd rather bet offshore where "no one's prying into my grocery bills alongside my flutter on the 2:30 at Newmarket."

And although the Commission insists these measures target harm hotspots, the collective data—65% refusal in one poll, 75% opposition in another—signals a revolt brewing, one that could redefine how UK punters engage with legal betting amid whispers of black market booms.

Conclusion

The convergence of survey data from the Betting and Gaming Council and the Gambling Commission lays bare a stark reality: UK bettors, from casual horse racing fans to frequent online players, largely reject handing over bank statements for affordability checks, with 65% and 75% opposition rates respectively underscoring the privacy-practicality clash at heart of these reforms; racing professionals' dire forecasts—£250 million industry hit, £200 million tax loss—amplify the stakes as black market shadows lengthen, all pointing toward pivotal adjustments before April 2026 rollout.

Observers note that while the push for safer gambling endures, the path forward demands balancing robust protections with user-friendly verification, lest regulated markets cede ground to unregulated rivals; in the end, this story highlights how finely tuned the UK's betting ecosystem remains, where one policy pivot could reshape punter habits, industry fortunes, and regulatory landscapes for years to come.