UK Gambling Commission Delays Full Rollout of Financial Risk Assessments After May 2026 Board Review

The UK Gambling Commission postponed its decision on the full implementation of Financial Risk Assessments following a board meeting held on 21 May 2026, and the move stems directly from the need for additional evaluation of pilot evidence gathered so far. Regulators cited incomplete data sets as the primary factor behind the extension, which affects a key component of the government’s 2023 Gambling Act white paper reforms designed as a harm-prevention mechanism. The decision arrives amid mounting pressure from multiple sectors that have voiced concerns over how these checks would operate in practice.

Background on the Proposed Reforms

Financial Risk Assessments were outlined in the 2023 white paper as a tool to identify customers who might be gambling beyond their financial means, and the framework called for operators to conduct checks using bank statements, payslips and other records once certain thresholds were crossed. Pilot programs began rolling out in selected environments to test data collection methods, customer response rates and operational feasibility, yet the results presented to the board in May 2026 revealed gaps that required further scrutiny before any nationwide mandate could proceed. Observers note that the assessments were intended to slot into existing responsible gambling protocols without creating unnecessary barriers for the majority of players who bet within their means.

The 21 May 2026 Board Decision

During the closed-door session on 21 May 2026 commissioners reviewed updated pilot statistics and concluded that additional assessment time was necessary before determining whether full implementation should move forward, and the official statement emphasized that no final timeline has been set. The postponement keeps the current voluntary and threshold-based pilot arrangements in place while more granular analysis continues, and this approach allows operators to maintain existing customer verification processes without immediate escalation. Those who have followed the regulatory timeline point out that similar evidence reviews have preceded other major policy adjustments in the past.

Stakeholder Opposition and Key Concerns

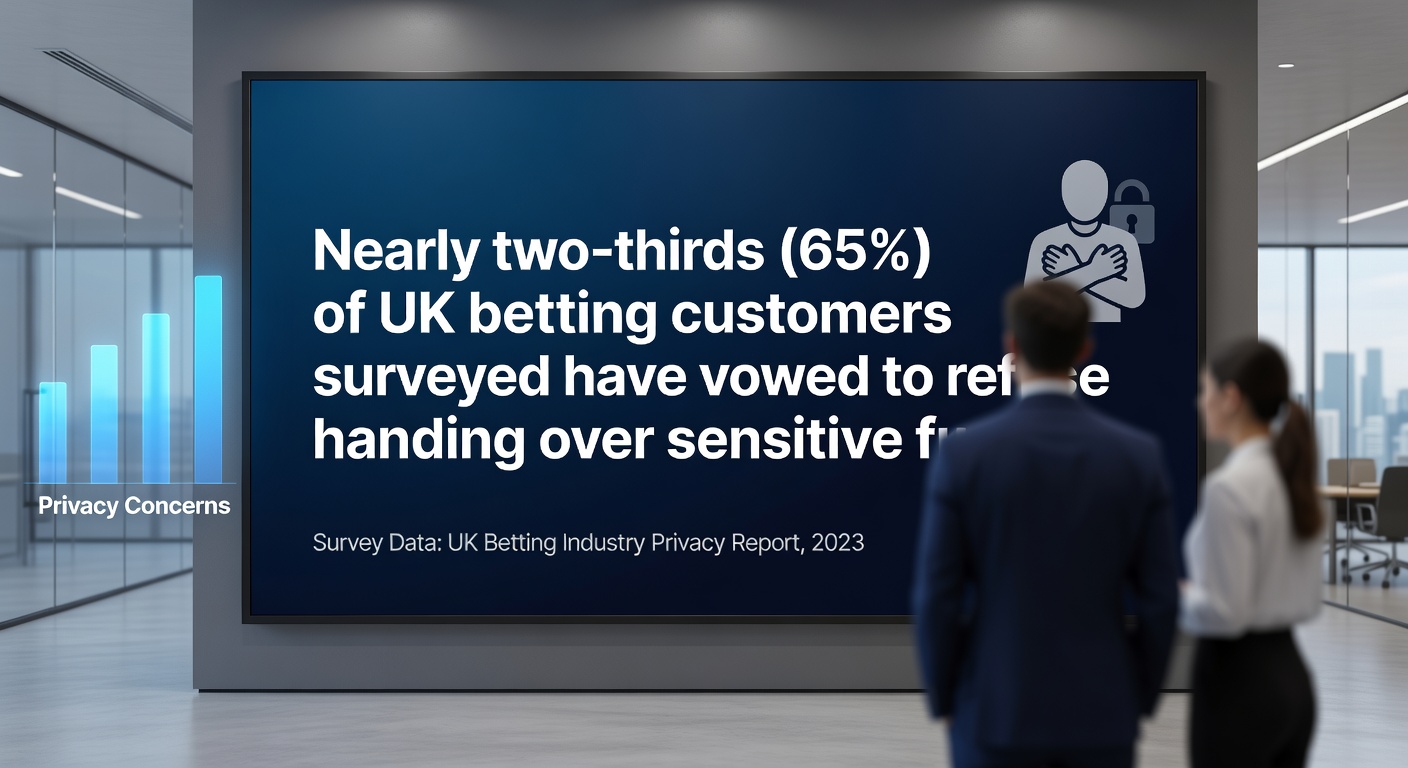

Growing opposition has come from gambling operators, cross-party MPs, the racing industry and several consumer groups, all of which have highlighted potential issues with customer friction, data reliability and the risk of pushing activity toward unregulated markets. Two-thirds of punters have indicated they would be unwilling to provide documents such as bank statements and payslips in order to continue betting, according to industry polling data, and this statistic has been cited repeatedly in submissions to the Commission. Operators argue that mandatory checks at lower thresholds could interrupt normal betting patterns for recreational customers, while racing representatives warn that reduced on-course and online turnover would directly affect prize money and breeding programs that rely on betting levies.

Data reliability remains another focal point because pilot evidence showed inconsistencies in how different banks format transaction information and how quickly verification systems can process requests during peak periods. Cross-party MPs have raised questions in parliamentary sessions about whether the assessments could inadvertently penalize customers whose income fluctuates seasonally, such as those in agriculture or performance industries, and they have requested clearer safeguards before any binding rules take effect. The black market risk has also featured prominently in submissions, with several trade bodies noting historical patterns where stricter verification in regulated markets coincided with increased traffic to offshore sites that operate without the same consumer protections.

Next Steps and Ongoing Evaluation

The Commission has indicated that further pilot work will continue through the remainder of 2026, with expanded sample sizes and refined data-sharing protocols between operators and financial institutions, and the goal is to produce a more comprehensive evidence base before any future board vote. Industry participants have been invited to submit additional operational feedback during this extended window, particularly around integration with existing age-verification and know-your-customer systems already in place. Regulators have stressed that the postponement does not signal abandonment of the policy but rather a commitment to ensuring any final framework rests on robust, tested foundations.

Conclusion

The 21 May 2026 decision keeps the Financial Risk Assessments framework in a holding pattern while additional evidence is gathered, and all parties involved continue to monitor pilot outcomes closely. Stakeholders across the betting, racing and political spectrum remain engaged in the consultation process, supplying data and operational insights that will shape whatever comes next. The extended timeline reflects the complexity of balancing harm-prevention objectives with practical implementation challenges that affect millions of customers and multiple sectors of the economy.